Welcome to the United Nations

Welcome to the United Nations

INTRODUCTION

The Addis Ababa Action Agenda identifies a set of commitments to mobilize resources to achieve the Sustainable Development Goals (SDGs) and calls for the alignment of public spending with national development priorities and the SDGs. In the context of the Fourth International Conference on Financing for Development (30 June-3 July 2025), discussions call for adopting a whole-of-government approach to ensuring transparency and accountability in public financial management and promoting budget transparency, accountability and efficiency, including enhancing oversight by Supreme Audit Institutions (SAIs).

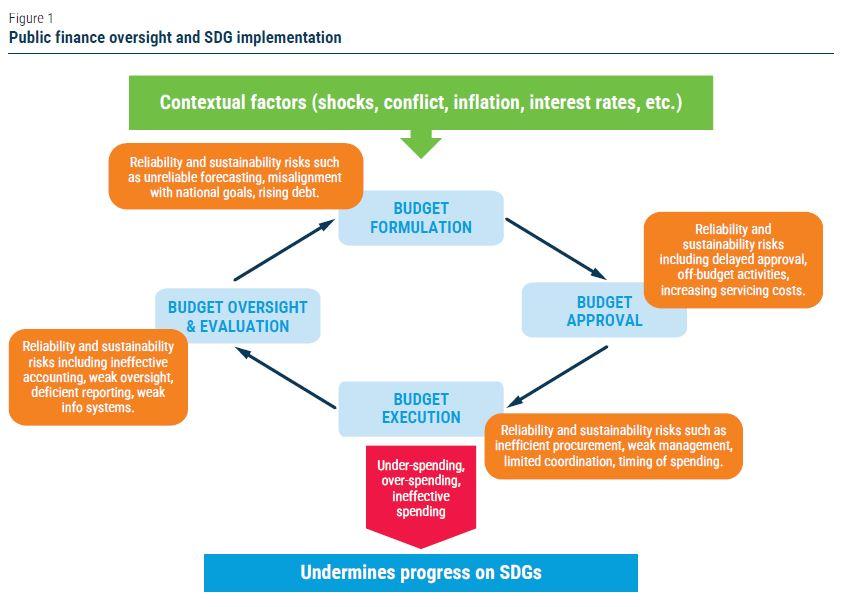

Public budgets are fundamental for the implementation of the SDGs. On the expenditure side, sound public financial management is needed for the effective and efficient use of resources. When budgets are not credible or implemented as intended, this impacts when and how essential services are delivered in areas such as health, education or the environment, and can undermine progress inaddressing poverty and inequality. Lack of credibility undermines public trust in institutions and jeopardizes the integrity of public funds, increasing corruption risks. SDG 16 recognizes the importance of budget credibility through a dedicated indicator (16.6.1) that measures the difference between the legislated annual budget and actual expenditure for the same year. Effectively delivering on the SDGs also requires that spending and revenue do not cause debt to rise continuously to ensure fiscal sustainability. SDG Target 17.4 recognizes the importance of long-term debt sustainability and reducing the risk of debt distress in developing countries.

SAIs audit public funds and government programmes to ensure that government revenue and spending are transparent and effective. Independent, evidence-based, and publicly available audit reports provide information on the performance of fiscal systems and how they contribute to the achievement of national priorities and the SDGs. This brief discusses how SAIs audit public finances and presents audit recommendations to improve the transparency and effectiveness of fiscal systems. It also identifies the barriers and opportunities for SAIs’ fiscal oversight to better inform the implementation and follow-up and review of the SDGs.

POSITIONING SAIS’ FISCAL OVERSIGHT WORK

While external oversight of fiscal systems still faces challenges, SAIs have gradually built their capacities to audit public finance. According to the INTOSAI 2023 Global Stocktake, 68 per cent of 166 SAIs audited public debt and 85 per cent audited tax and revenue collection in 2020-22, and 87 per cent of respondents conducted audits on COVID emergency spending. This significance also holds for the least developed countries (LDCs) and small island developing States (SIDS). SAIs in SIDS, for example, reported their highest number of audits on emergency spending and taxes and revenues during that period. Similarly, 74 per cent of 27 respondents to a 2021 SAI survey conducted by UN DESA and the International Budget Partnership (IBP) identified budget credibility as a significant problem in their countries and 82 per cent of respondents addressed related issues in their work.

SAIs assess various fiscal issues in their reports. Some audits take a systemic, whole-of-government approach, focusing on transversal (cross-cutting) public financial management processes, while others focus on specific entities or programmes. Topics audited include the fiscal, legal and governance framework, financial planning and budget preparation, budget and debt approval, execution and implementation, and monitoring and oversight. While public finance audits are generally not explicitly linked to the implementation of the SDGs nor to specific targets, there are some exceptions. For example, the 2023 Annual Report of SAI Austria underlines its aim to ensure a whole-of-government view on public finances that contributes to SDG 16.6. Similarly, SAI Kenya has referred to specific SDG targets in the rationale of audits on public debt.

CHALLENGES AND OPPORTUNITIES FOR STRENGTHENING FISCAL SYSTEMS

SAIs recognize the implementation of measures to improve debt management, strengthen fiscal legal and organizational frameworks, enhance risk management and ensure fiscal sustainability. SAIs have also highlighted compliance with fiscal laws and regulations and the fair presentation of countries’ fiscal and debt positions. For example, SAI Finland and UK found that the respective debt management strategies are well established and have been operating effectively even in times of crisis. SAI Kenya noted that the National Treasury has put in place measures aimed at enhancing public debt management, including an amendment to the Public Financial Management Bill to have the debt limit approved by the Parliament and ensure that it is anchored in sustainability.

Despite these advances, SAIs identify opportunities for strengthening fiscal systems. Audits have recommended sustainable reforms aligned with long-term fiscal objectives. SAI Germany, for example, recommended systematically highlighting sustainability aspects in budget planning and linking them with relevant budget titles. SAI Korea recommended addressing inefficiencies in public spending, such as unwarranted subsidies and ineffective programs, to reduce unnecessary expenditures and improve budget execution.

In developing countries, SAIs have made recommendations to improve legal frameworks and adherence to legislation, set clear institutional roles, and improve procedures. For example, SAI Sierra Leone made recommendations related to legal and organizational arrangements, including the timely preparation of borrowing plans aligned with the medium-term debt strategy, the finalization of procedural manuals, and ensuring legislative approval of all external loan agreements according to the Public Debt Management Act.

SAIs have emphasized the importance of developing fiscal and debt strategies and facilitating institutional coordination to support fiscal sustainability and more efficient debt management. The U.S. Government Accountability Office (GAO) recommended that Congress develop a plan to address the unsustainable fiscal path, emphasizing that a sustainable fiscal policy would lead to debt held by the public growing at the same -or slower-rate than the economy.

There are also opportunities to address transversal risks related to fiscal monitoring, evaluation and supervision. Audits (e.g., Brazil, Georgia, Morocco, Seychelles, UK) highlight the need to enhance timely monitoring and improve tracking and evaluation of debt management. Audits identify problems in systems to capture and manage performance information to inform the budget process such as lack of targets, insufficient or inappropriate indicators, adhoc monitoring activities and inability to link expenditures and financial indicators to performance indicators (e.g., Colombia, Costa Rica, Ghana, Netherlands, New Zealand, the Philippines).

SAIs have recommended enhancing regular and reliable fiscal reporting to provide stakeholders with clear, complete and understandable information (e.g., Brazil, India, Maldives, Peru, UK). Limited transparency, incomplete or poor information, and reporting problems undermine a proper assessment of government finances, affecting the credibility of budgets. For example, the Netherlands’ Court of Audit found that budget documents often failed to include information on expenditure plans, policy goals and achievements, and policies with responsibilities shared across sectors, making it difficult to assess whether spending had proceeded according to plan and results matched budget execution.

In SIDS and LDCs, audit recommendations reflect particular development challenges such as increasing constraints in some countries’ fiscal space. In its review of the medium-term fiscal strategy 2024-26, for example, the Auditor-General of the Maldives called for enhanced transparency and accountability and required the Ministry of Finance to explain the reasons for deviating from previous fiscal objectives and to report annually to Parliament on the actions taken to implement the recommendations of parliamentary committees and the Auditor General on the fiscal strategy report.

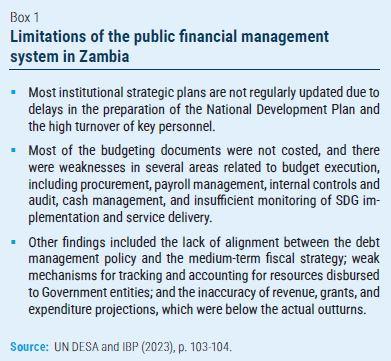

Audit reports in LDCs have also highlighted capacity constraints, which affect record keeping, budget execution, contracting of loans, the use of debt funds and project implementation. To address these challenges, SAIs call for strengthening fiscal responsibility and debt management, enhancing monitoring and evaluation, improving coordination, planning and record keeping. See Box 1 on the example of Zambia.

THE IMPACT OF EXTERNAL AUDITS ON FISCAL SYSTEMS

Public finance audits create public value directly – through the effective implementation of audit recommendations by audited entities - and indirectly – through other stakeholders that leverage audit information and findings. Engagement and productive collaboration between the SAI and government entities is key.

SAIs have taken steps to address these challenges and strengthen collaboration with stakeholders and incentivize executive and legislative action on audit findings and recommendations. For example, Pacific SAIs (e.g., Fiji, Solomon Islands, Tonga) have enhanced collaboration with the respective Public Account Committees by developing frameworks and procedures for review and scrutiny of external audit reports and training legislators. In Georgia, the SAI, legislators and the auditees have access to the electronic system that integrates audit reports, the corresponding recommendations, and the action plans for implementing them, and legislators can independently follow up with government entities on the implementation of recommendations. The use of this system helped increase the implementation rate of audit recommendations from 43 per cent in 2015-2017 to 60 per cent in 2018-2019.

There are positive examples of audit impact on fiscal systems. Audits have resulted in the modernization of government accounting and better alignment with international standards (e.g., Ireland), improved reporting, coordination and accountability (e.g., Yemen), enhanced alignment with the SDGs (e.g., Egypt), and improved legal frameworks (e.g., Argentina), among other positive effects. In Portugal, for example, the implementation of audit recommendations has led to improved budget documents and better reporting on tax expenditure, the creation of new technical units, a new accounting framework for the social security accounts, improved inventory of real estate assets, and improved SDG governance, including a better link between goals, actions and allocated financial resources in the 2024 budget.

Internal challenges for advancing fiscal oversight revolve around SAI capacities, resources, organizational settings, and the impact of these factors on the timeliness and opportunity of public finance audits. External challenges relate to lack of access to timely and reliable fiscal information and data, constraints in internal oversight functions, the lack of collaboration among public finance stakeholders, and the novelty of performance audits on public finance in some countries. The political nature of budget processes, changing political landscapes, and asymmetries in accountability ecosystems also affect SAIs’ work. Delays (or omissions) in the approval of audit reports on budget execution or public debt by the legislature, for example, have a negative impact, as public finance audits are only useful if they are timely enough to allow potential problems to be addressed.

SAIs and auditors also identify opportunities for strengthening fiscal oversight. The recognition of SAIs’ oversight role on public finance, the accumulated experience and documentation of good practices, the recurrent nature of budget oversight work, ongoing learning, improvements in budget information and data, and advancements in data analytics and ICTs, among other factors, open opportunities for more robust SAI work. Collaboration among SAIs and with other stakeholders is also seen as an opportunity to enhance SAI capacities and the impact of fiscal oversight.

WAY FORWARD

Effective and transparent public financial management is crucial for building trust in public institutions and mobilizing and effectively spending additional resources for sustainable development. SAIs provide critical information and evidence to inform assessments of the performance of national fiscal systems, including in relation to SDG implementation, and to enhance the effectiveness of fiscal systems for sustainable development.

Unlocking the contribution of SAIs can be supported through specific actions. First, it is important to raise awareness of fiscal oversight work by documenting and sharing SAI experiences and communicating the results of audits. Advancing performance audits on public finance or combining performance with other audit methodologies, and more systematic engagement with stakeholders around budget evaluation and oversight can also help enhance the impact of audits. SAIs can also add value by complementingcomprehensive, systemic audits with audits on specific risks at programme or entity levels. Finally, there are opportunities to strengthen the linkages between public finance and performance audits at the sector level, and to more directly link public finance audits with national priorities and SDGs. Audits on areas such as climate change, the environment, and gender, among others, provide opportunities in this direction.