Welcome to the United Nations

Welcome to the United Nations

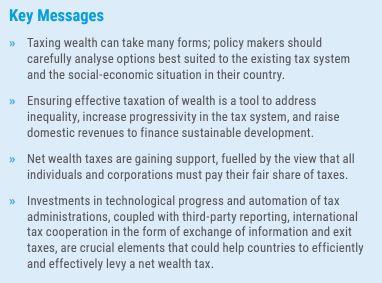

Wealth inequality, i.e. the distribution of wealth across the global adult population, is persistently high. Since 1995, global net wealth per adult has grown around 3.2% per year, though at varying rates across different population groups. Wealthier individuals have experienced faster increases in their wealth compared to those with less wealth. This has resulted in a stark imbalance: the poorest half of the world’s population currently owns just 2% of global wealth, whereas the richest half owns 98%. This inequality is even more concentrated at the top, with the wealthiest 1% owning 38% of total wealth and the top 0.1% owning 19%, further widening the gap between the richest and the rest of the world.

The COVID-19 pandemic brought a sharp rise in extreme poverty leading to increases in wealth inequality within countries. The global pandemic also led to the largest rise in between-country inequality in three decades and an increase in global inequality for the first time since 1990.

Widening inequality has significant implications for economic growth. A country’s per capita gross domestic product (GDP) growth rate has been shown to slow down above a certain level of inequality as a skewed distribution of income and wealth can affect aggregate demand. In contrast, an increase in the income share of the bottom 20% is generally associated with higher GDP growth.

Reducing inequality is essential to ensuring that sustainable development efforts benefit all, especially those furthest behind. Reducing inequality is a global goal: Sustainable Development Goal (SDG) 10 aims to reduce inequalities in different areas, including income and wealth. The global trend towards the concentration of wealth and income also negatively impacts poverty reduction measures and threatens the pace of social and economic development. Inequality has also been shown to be linked to increased crime and exposure and vulnerability to environmental degradation. The reduction of inequalities, both within and between countries, is a pre-requisite for achieving the 2030 Agenda for Sustainable Development and the SDGs.

Reducing inequality is also pivotal for social cohesion. The perception that some companies and individuals are evading or avoiding taxes has increasingly put a strain on the relationship between citizens and their governments. United Nations Secretary-General António Guterres acknowledged this strained relationship in his report “Our Common Agenda” and has called for the establishment of a new social contract and a new global deal that “create[s] equal opportunities for all and respect[s] the rights of all” in order to overcome global inequality. He highlighted that taxation must play a role in this new social contract, stating that “everyone – individuals and corporations – must pay their fair share”. Both the new contract and the global deal should be rooted in the 2030 Agenda.

Public opinion is increasingly favouring the taxation of wealth. Available survey data shows broad public support for tax increases on high earners. On the occasion of the 18th annual G20 Summit in September 2023, a coalition of NGOs published an open letter, signed by economists, millionaires, and political representatives, calling on G20 countries to work together to enact new tax regimes - at national and international levels - that eliminate the ability of the ultra-rich to avoid paying their dues, and introduce higher taxes on those with extreme wealth. In July 2024, G20 leaders committed in the Rio de Janeiro Leaders’ Declaration to engage cooperatively to ensure that ultra-high-net-worth individuals are effectively taxed.

Tax policy is crucial to address inequality. Taxes can target the entire income distribution, including through progressive taxation of high incomes and wealth. If designed and administered successfully, taxes on wealth can yield substantial tax revenue, contributing to efforts to containing the rise of extreme wealth inequality, and helping to mitigate the potentially negative impact of extreme wealth concentration. However, over the past decades, tax rates on wealth have generally declined across the world.

There is a new openness to explore the taxation of wealth as a policy instrument to finance the SDGs while reducing income and wealth inequality. Recently, some countries have introduced new taxes on wealth such as Bolivia in 2020, or levied one-off solidarity taxes in response to the COVID-19 pandemic such as Argentina. In several other countries, there have been detailed proposals and ongoing discussions about implementing net wealth taxes (such as in the UK or Chile). The UN Committee of Experts on International Cooperation in Tax Matters recently published a Handbook on Wealth and Solidarity Taxes and the G20 committed to cooperative engagement on ultra-high-net-worth individuals.

HOW CAN WEALTH BE TAXED?

Wealth taxation can take many different forms, such as taxes on capital income, taxes on the transfer of wealth or taxes on the stock of wealth, including net wealth taxes. Taxes on wealth differ in terms of their advantages and disadvantages depending on tax policy design choices (exemptions, rates, etc.), the existing tax system, the administration of the tax as well as the socio-economic context of a country.

Taxes on capital income are levied on interest income, dividends, certain types of royalties, income from real estate and capital gains, i.e., the difference between the purchase and selling price of assets, including stocks, real estate, art and jewellery taxing the appreciation of assets at the time of selling. Taxes on the transfer of wealth can take the form of inheritance, estate or gift taxes. In addition to net wealth taxes, taxes on the stock of wealth include property taxes levied regularly on the value of the property. An alternative to a comprehensive net wealth tax are so-called wealth tax add-ons. Examples include a surtax on real estate or a presumptive tax on financial assets. Taxes on the stock of wealth can also take the form of “solidarity taxes” that are introduced in response to a specific event or crisis. For example, Ecuador implemented a one-time net wealth tax to raise revenue to rebuild the country in the aftermath of the 2016 earthquake.

This policy brief will focus on net wealth taxes, which are typically levied annually on an individual’s net worth – i.e. total assets, including financial and non-financial assets, net of all debts. The brief outlines the advantages and disadvantages of net wealth taxes, lays out some policy instruments that help in their administration, and explains why and how international tax cooperation can aid countries in successfully levying net wealth taxes.

WHAT ARE ADVANTAGES AND DISADVANTAGES OF NET WEALTH TAXES

Net wealth taxes have several potential advantages. First, the revenue collected from a net wealth tax, if properly invested, can foster sustainable development, help reduce wealth inequality, and promote equality of opportunity. By taxing net wealth in addition to income, the tax system can become more progressive and better capture taxpayers’ ability to pay.

Furthermore, a net wealth tax can also be more comprehensive compared to other forms of wealth taxation, such as a capital income tax, since the tax is levied irrespective of whether assets generate a financial return. This means that the tax is generally applied to productive and non-productive assets, which may incentivize taxpayers to direct their investments towards higher-return productive assets that could boost the economy and benefit the entire population.

Another advantage of net wealth taxes is that they are generally levied on an accrual basis, i.e., based on the market value of the assets, rather than triggered by a transaction or sale. This approach avoids a “lock-in” effect – where taxpayers avoid selling assets like property to avoid capital gains taxes. By taxing appreciated assets on the basis of the taxpayer’s current wealth, net wealth taxes can enhance fairness in the system. They can also raise revenues in volatile economic environments, thereby stabilizing a countries’ tax revenues.

However, net wealth taxes also have disadvantages, which has eventually led many countries to abandon these taxes. The number of OECD member countries levying a net wealth tax declined from 12 in 1990 to only 4 in 2024. Many of them citing that the administrative burden of the tax was too high vis-à-vis the revenues generated. Where still employed, wealth taxes are not a relevant source of revenue due to high exemption thresholds, tax evasion, and enforcement challenges.

A common reason for eliminating net wealth taxes in the past was the tax’s high administrative cost vis-à-vis its impact on inequality levels. In fact, one of the factors that can be an advantage for a net wealth tax, i.e. the taxation on an accrual basis, can lead to inefficient or inequitable outcomes, as actual cash flow is not taken into account and taxpayers with illiquid assets may not be able to easily pay the tax. Moreover, net wealth taxes can create distortions in economic behaviour by reducing the incentive to save. While net wealth taxes may incentivize investments in higher-return productive assets, net wealth taxes may encourage taxpayers to invest in liquid assets. Since net wealth taxes are levied on assets net of debts, taxpayers may offset their taxable wealth by borrowing against such assets, reducing their overall tax liability. This behaviour could discourage long-term investments, potentially reducing the overall efficiency in capital allocation.

Valuing wealth accurately is also often cited as a challenge for a net wealth tax, especially where valuation techniques are overly complicated and / or where net wealth tax returns are entirely dependent on self-reporting by taxpayers. Additionally, net wealth taxes may lead to economic “double taxation”, whereby taxpayers are subject to multiple tax obligations on the same elements of wealth. This could happen, for example, when they are taxed by different tax authorities or through different taxes.

Political obstacles can also impact the enactment or implementation of net wealth taxes, especially in cases where the tax would lead to higher taxes for politicians who have to legislate on such issues, or individuals that contribute to the politicians’ campaigns. A significant challenge can also be political influence of wealthy individuals or groups, who can use their resources to lobby against such measures. Where net wealth taxes lack strong political backing, allow for many exemptions, or are levied at very low rates, they often fail to generate sufficient revenue to justify their administration.

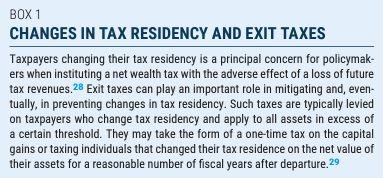

A significant risk associated with net wealth taxes is that taxpayers change their tax residency. The introduction of such taxes may prompt wealthy individuals to change their tax residence to avoid the tax, which could lead to base erosion. This risk is particularly high when individual countries adopt wealth taxes without mitigating this risk through, for example, exit taxes discussed below or without broader international cooperation.

DESIGN CONSIDERATIONS FOR A NET WEALTH TAX

A starting point for policy makers seeking to reduce inequality and / or raise revenue for investment in sustainable development is to carefully analyse the potential benefits of a net wealth tax vis-à-vis its administrative costs. Here, the tax base and the tax rate should be taken into account along with anticipated tax avoidance behaviour. Existing taxation of wealth and other rules that would have an impact, such as exit taxes or valuation rules, should also be considered.

There are different approaches to fiscally addressing wealth inequality and enhancing revenue collection. In some cases, introducing new wealth taxes to target previously under-taxed forms of wealth may be more effective. However, in other cases, reforming existing taxes to ensure their effectiveness might be a more practical solution, particularly where administrative capacity is limited. While new taxes could provide novel solutions, reforming the existing tax system is often more administratively feasible and less disruptive to the existing fiscal framework.

When implementing a net wealth tax, key design considerations include tax rates, wealth brackets, and covered assets. While low rates and narrow tax bases may not justify administrative costs, high rates on mobile assets risk tax avoidance through changes in tax residency. Countries must calibrate these elements based on their tax systems and enforcement capabilities. The choice of wealth threshold is also important—too low creates an administrative burden and affects lower-income earners, while too high limits revenue. However, thresholds can enable tax avoidance through asset undervaluation or strategic wealth distribution, which makes robust anti-avoidance measures crucial.

Many of the issues mentioned above can be addressed through tax policy design choices, considering the factors that have impacted countries’ ability to successfully levy wealth taxes in the past. Net wealth taxes were often too complex, e.g., allowing for too many exemptions and / or relying on complicated valuation techniques to estimate an individual’s wealth. This, in turn, opened the door to tax planning strategies and ultimately resulted in heightened tax avoidance and evasion. Likewise, due to their complexity, net wealth taxes were difficult to administer, resulting in governments incurring high auditing costs to enforce them. Moreover, limited international cooperation made it hard for tax administrations to successfully audit crossborder tax planning strategies.

Where countries failed to anticipate the behavioural response from wealthy individuals to the implementation of wealth taxation measures, the effectiveness of the net wealth tax has been negatively impacted. It is pivotal to anticipate changes in investment behaviour, aggressive tax and financial planning and changes in tax residency to effectively address these challenges. See Box 1 for more information on exit taxes.

IS THE TIME RIPE FOR THE INTRODUCTION OF NET WEALTH TAXES?

Although net wealth taxes have faced obstacles in the past, recent developments have fostered an environment more conducive to their adoption and success.

First, there is growing concern among governments and their citizens about inequality, coupled with heightened interest in the fairness of tax systems. Scandals such as the Pandora, Paradise, and Panama Papers have exposed the tax planning strategies of high-net-worth individuals and companies alike. Citizens increasingly demand that wealthy individuals contribute their fair share of taxes to finance sustainable development. As a result, there is pressure on governments to enact taxes that are easy to apply and enforce with fewer exceptions and loopholes. Failing to do so could further erode citizens’ trust in their tax system and in their governments.

Second, technological advancements have led to the use of increasingly sophisticated IT tools in tax administrations, allowing for more efficient tax administration and audits. Automation helps streamline routine processes such as data collection and cross-verifying taxpayer information, which reduces opportunities for corruption and profit-seeking within tax systems. Additionally, technology enhances enforcement, making it easier for tax authorities to detect underreporting and enforce compliance, even across borders. Investment in technology and virtual infrastructure as a result of the COVID-19 pandemic has significantly aided the automation of tax structures and allowed for tax administrations to be better equipped to administer taxes and audit taxpayers.

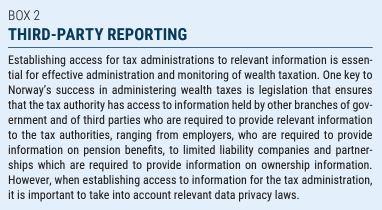

Third, international cooperation is key to the effective implementation of net wealth taxes. Global cooperation can help mitigate issues such as tax residency changes by promoting administrative assistance in these cases among countries. Additionally, such cooperation can give tax administrations access to information needed to audit net wealth taxes. Tax transparency mechanisms have enabled the sharing of relevant tax information between countries, which is crucial in auditing high-net-worth individuals. In addition, some tax authorities have improved their access to data held by third parties, from both the public and private sector, which has, in turn, improved the possibilities for administration and monitoring of wealth taxes (see Box 2 below).

CONCLUSION

The convergence of technological advancement, increased public interest in, and support of, and increased tax transparency has created a new window of opportunity for implementing effective net wealth taxes. There is also openness to even stronger international cooperation to counter tax evasion and avoidance in this area. All of these developments can help ensure that net wealth taxes fulfil their core purpose of reducing inequality while generating revenues for sustainable development.