Welcome to the United Nations

Welcome to the United Nations

Recurrent crises are affecting SDG progress and outlook

Recurrent crises are affecting SDG progress and outlook

SDG progress has been set back, and the outlook faces uncertainty given the cumulative and amplified impacts of the COVID-19 pandemic, the war in Ukraine and climate change. This brief examines the channels through which these three shocks are impacting the SDGs and their implications for the achievement of the 2030 Agenda for Sustainable Development through recurrent crises. COVID-19 is estimated to have caused nearly 15 million deaths globally and brought the economy and people’s lives to a standstill for long periods in many parts of the world. The pandemic and the containment measures to control it significantly slowed economic growth, increased unemployment, raised poverty and hunger, widened inequality, and caused additional adverse impacts on women and children in many countries around the world. With uneven access to vaccines and treatments, and the continuing emergence of new variants, the pandemic continues to exert a malign influence on sustainable development. The war in Ukraine has led to a humanitarian emergency, accompanied by a global food and energy shock, upending a fragile economic recovery from the pandemic. The war has placed additional pressures on the post-pandemic recovery of developing countries that were already at a significant disadvantage. It is projected to lower economic growth worldwide and further exacerbating debt burdens for many developing countries. Sharp increases in the prices of fuel, food, fertilizer and selected metals/minerals have been key in the global transmission of impacts. Climate change continues unabated, increasing the frequency and intensity of extreme weather events across the world, besides resulting in longer-term damage such as prolonged drought and rising sea levels. There is now a 50:50 chance of the annual average global temperature temporarily reaching 1.5° C above the pre-industrial level for at least one of the next five years (WMO 2022). Global greenhouse gas emissions need to peak before 2025 at the latest and be reduced by 42 per cent by 2030, while methane also needs to be reduced by about a third in the same period, to stay within reach of the 1.5° C target (IPCC 2022). Crises such as these amplify one another and weaken the capacity of countries to respond. The effects of the three recurrent crises are exacerbated by other more localized ones, including droughts and floods, continuous conflicts in various parts of the world, and smaller outbreaks such as avian influenza. This confluence puts countries in a perpetual crisis mode, with limited room to recover and invest in sustainable development.

Headwinds in an increasingly turbulent world

Shocks are transmitted simultaneously through multiple channels

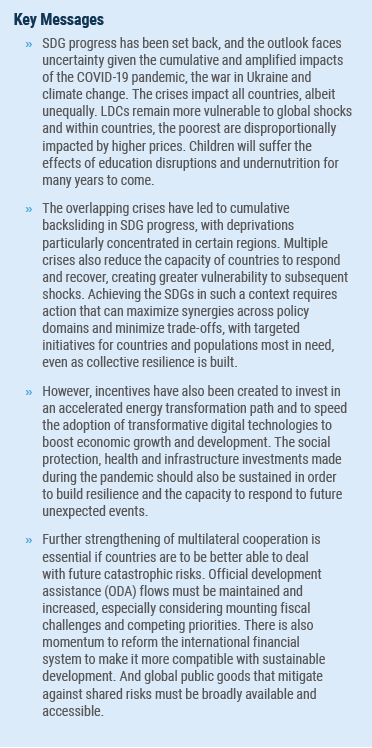

The fragile economic recovery from COVID-19 has been upended by the war in Ukraine. In early 2022, an uneven economic recovery was underway, with the UN expecting the global economy to grow by 4.0 percent in 2022 (UN DESA 2022b). The recovery was expected to be threatened by “new waves of COVID-19 infections, persistent labor market challenges, lingering supply-chain challenges and rising inflationary pressures.” However, in May 2022, the global growth projection was revised to 3.1 per cent, driven significantly by the war in Ukraine. The downgrades in growth prospects are broad-based, including the world’s largest economies and the majority of other developed and developing countries, with commodity-importing developing economies particularly hard hit. As countries seek to contain inflation, the rapid economic recovery experienced in 2021 has begun to fade. Compared to the pre-pandemic forecasts, the shortfall of global income between 2020 and 2030 will amount to $34 trillion (Figure 1). The gross world product in 2030 will be 5.31 per cent below the pre-pandemic forecast. This projected drop in global GDP poses risks for SDG implementation.  Rising inflationary pressures imperil both economic growth and SDG implementation. Global inflation is projected to rise to 6.7 per cent in 2022, twice the average of 2.9 per cent during the 2010-2020 period, with a sharp increase in food and energy prices, disproportionately impacting the poor. As central banks raise interest rates to tame inflation, economic growth slows further. Tighter monetary policy in advanced economies could also lead to capital outflows from developing economies, a deterioration in public finances and higher debt distress risks just as countries need to invest in SDG implementation. Measures such as export controls may provide some price relief for the local population but when undertaken by major food exporters, can contribute to keeping global prices elevated, Agricultural production is also threatened by more localized events such as prolonged droughts and avian influenza, adding to inflationary pressures. Global trade, supply chains and transportation costs are experiencing considerable shocks. Global trade fell by 9.6 per cent in 2020 (by 12 per cent in LDCs) during the pandemic. Freight transport costs also increased by close to 350 per cent between May 2020 and June 2021. Rising fuel prices from the war in Ukraine have added to the pressures on transport costs. A hyper-connected global economy with geographically dispersed production in global value chains can imply greater vulnerability of manufacturing and distribution to separate shocks. While the worldwide trade in goods was back to its pre-pandemic levels by the end of 2022, supply chains have again been disrupted by the war in Ukraine, affecting prices and the availability of goods. Global employment remains well below pre-pandemic levels. Recent job creation has not caught up with employment losses from the pandemic, but with differences across regions. While labor markets in developed countries were gradually improving with economic recovery, employment growth in developing countries was anemic amid lower vaccination rates and limited stimulus spending. A return to pre-pandemic labor market performance was already unlikely for much of the world over the coming years, and the trend is further exacerbated by the declining economic prospects since February 2022. An estimate from January 2022 indicated that global working hours in 2022 would be almost 2 per cent below their pre-pandemic level, reflecting a deficit of about 52 million full-time equivalent jobs (ILO 2022). In May 2022, the forecast for the global unemployment rate in 2030 was revised upward to 6.6 percent, reflecting the challenges that have accumulated since January 2020 when the forecasted value was 5.4 per cent. Remittance flows, a significant source of income for many developing country households, have become less reliable. Global remittances declined in 2020 due to the pandemic but recovered in 2021 in line with economic activity. A protracted and uncertain economic recovery in source countries makes future remittance outflows more unpredictable. The exception may be in commodity-exporting countries benefiting from high global prices, from which regular remittances outflows may still serve to soften food insecurity and financial constraints in recipient countries.

Rising inflationary pressures imperil both economic growth and SDG implementation. Global inflation is projected to rise to 6.7 per cent in 2022, twice the average of 2.9 per cent during the 2010-2020 period, with a sharp increase in food and energy prices, disproportionately impacting the poor. As central banks raise interest rates to tame inflation, economic growth slows further. Tighter monetary policy in advanced economies could also lead to capital outflows from developing economies, a deterioration in public finances and higher debt distress risks just as countries need to invest in SDG implementation. Measures such as export controls may provide some price relief for the local population but when undertaken by major food exporters, can contribute to keeping global prices elevated, Agricultural production is also threatened by more localized events such as prolonged droughts and avian influenza, adding to inflationary pressures. Global trade, supply chains and transportation costs are experiencing considerable shocks. Global trade fell by 9.6 per cent in 2020 (by 12 per cent in LDCs) during the pandemic. Freight transport costs also increased by close to 350 per cent between May 2020 and June 2021. Rising fuel prices from the war in Ukraine have added to the pressures on transport costs. A hyper-connected global economy with geographically dispersed production in global value chains can imply greater vulnerability of manufacturing and distribution to separate shocks. While the worldwide trade in goods was back to its pre-pandemic levels by the end of 2022, supply chains have again been disrupted by the war in Ukraine, affecting prices and the availability of goods. Global employment remains well below pre-pandemic levels. Recent job creation has not caught up with employment losses from the pandemic, but with differences across regions. While labor markets in developed countries were gradually improving with economic recovery, employment growth in developing countries was anemic amid lower vaccination rates and limited stimulus spending. A return to pre-pandemic labor market performance was already unlikely for much of the world over the coming years, and the trend is further exacerbated by the declining economic prospects since February 2022. An estimate from January 2022 indicated that global working hours in 2022 would be almost 2 per cent below their pre-pandemic level, reflecting a deficit of about 52 million full-time equivalent jobs (ILO 2022). In May 2022, the forecast for the global unemployment rate in 2030 was revised upward to 6.6 percent, reflecting the challenges that have accumulated since January 2020 when the forecasted value was 5.4 per cent. Remittance flows, a significant source of income for many developing country households, have become less reliable. Global remittances declined in 2020 due to the pandemic but recovered in 2021 in line with economic activity. A protracted and uncertain economic recovery in source countries makes future remittance outflows more unpredictable. The exception may be in commodity-exporting countries benefiting from high global prices, from which regular remittances outflows may still serve to soften food insecurity and financial constraints in recipient countries.

Impacts disproportionately harm the most vulnerable

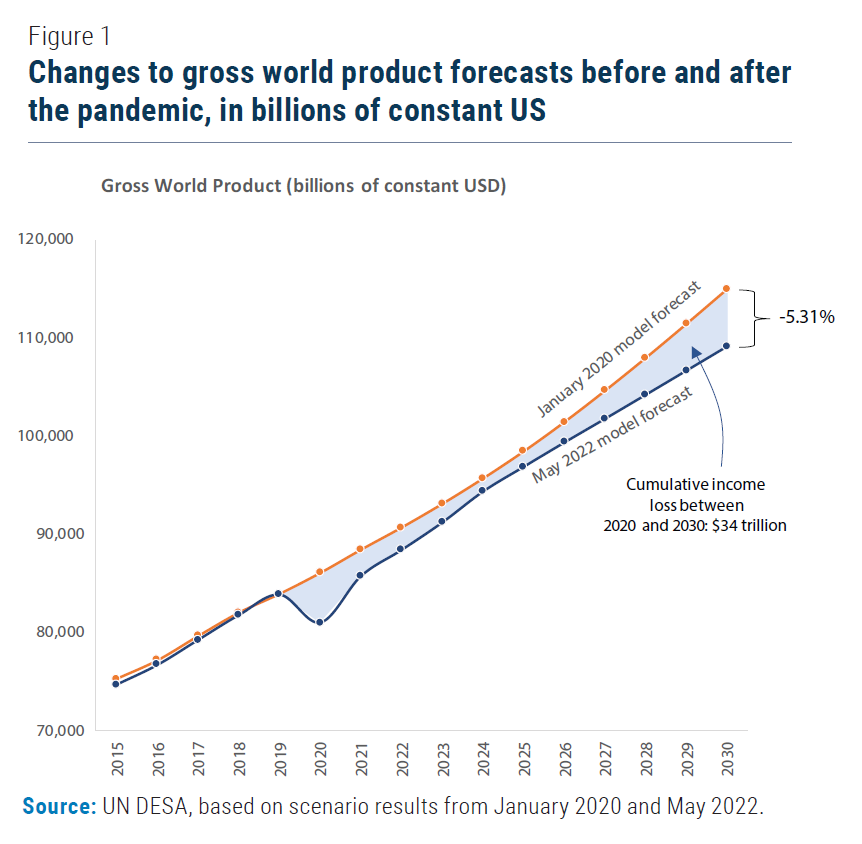

The impacts of the multiple crises will be felt in all countries, but through different channels and with different levels of magnitude. Several factors, such as a country’s export structure and integration in the global trading system, debt burdens, fiscal space, existing levels of SDG achievement and susceptibility to climate and other shocks, will all be important factors. The pandemic did little to change the growing concentration of poverty in sub-Saharan Africa. The pre-pandemic general decline in poverty was interrupted in 2020 with substantial increases in the number of poor in South Asia (Figure 2). Unfortunately, the number of people living in extreme poverty will continue to rise in sub-Saharan Africa and by 2030 the region is projected to be home to 83 per cent of the world’s poor, or 477 million people. The ratio of poor to total population in the region will have declined from 37 per cent in 2019 to 28 per cent in 2030, but much faster progress is needed to reduce the number of poor and achieve the 2030 goal of eradicating poverty.  Least developed countries were more severely affected by the pandemic given their less diversified exports and higher dependency on commodities (UN DESA 2021b). LDC exports of goods decreased by 12 per cent in 2020, as mentioned earlier. The value of commercial services in LDCs declined even more sharply, or by 35 per cent in 2020, while in the rest of the world the decline was 20 per cent. The war in Ukraine is now aggravating the situation in many LDCs, as they are generally more vulnerable to external shocks, particularly because some are net importers of food and energy. In these countries, it is expected that the compounding effects of these shocks may have long-lasting negative effects on different dimensions of sustainable development. Within countries, individuals and households are also affected to different degrees. COVID-19 started a vicious cycle whereby disadvantaged groups were not only more exposed to immediate risks from the pandemic, but also less prepared to cope with the financial burdens of the lockdowns (UN DESA 2021c). Poorer countries are still denied equitable access to vaccines and treatments. In addition, the war in Ukraine, in a worst-case scenario, can cause an additional 11 million people to fall into poverty (UNDP 2022). Rising food and energy prices will disproportionately affect the most vulnerable. These essentials make up a larger share of the consumption basket of the poor, so an increase in their prices disproportionately erodes the real income of such households. They may also have less access to financing options to absorb such price increases. Lower-income households also rely more on wages, transfers, and pensions which typically lag behind price inflation. At the same time, high food prices could increase the returns to agriculture, potentially improving the incomes of those working in this sector. Long-term impacts on children are likely to be severe, particularly in developing countries. It is estimated that 147 million children missed more than half of their in-class instruction during the past two years. The share of 10-year-old children in low – and middle-income countries lacking reading proficiency rose from 59 to 63 per cent, with a similar shift also experienced in math proficiency. This effect will linger as this generation of students could lose $17 trillion in lifetime earnings at present value, the equivalent of 14 per cent of today’s gross world product. They are also getting less support as 65 per cent of governments in low – and lower-middle-income countries reduced their education budget. The 2007-2008 food price crisis also showed how spikes in food prices increased malnutrition among the poor, with lasting consequences. Soaring food prices adversely affected child development through poorer nutrition – potentially leading to irreversible loss in cognitive abilities and other lifelong disadvantages – among households that were not able to produce food for home consumption.

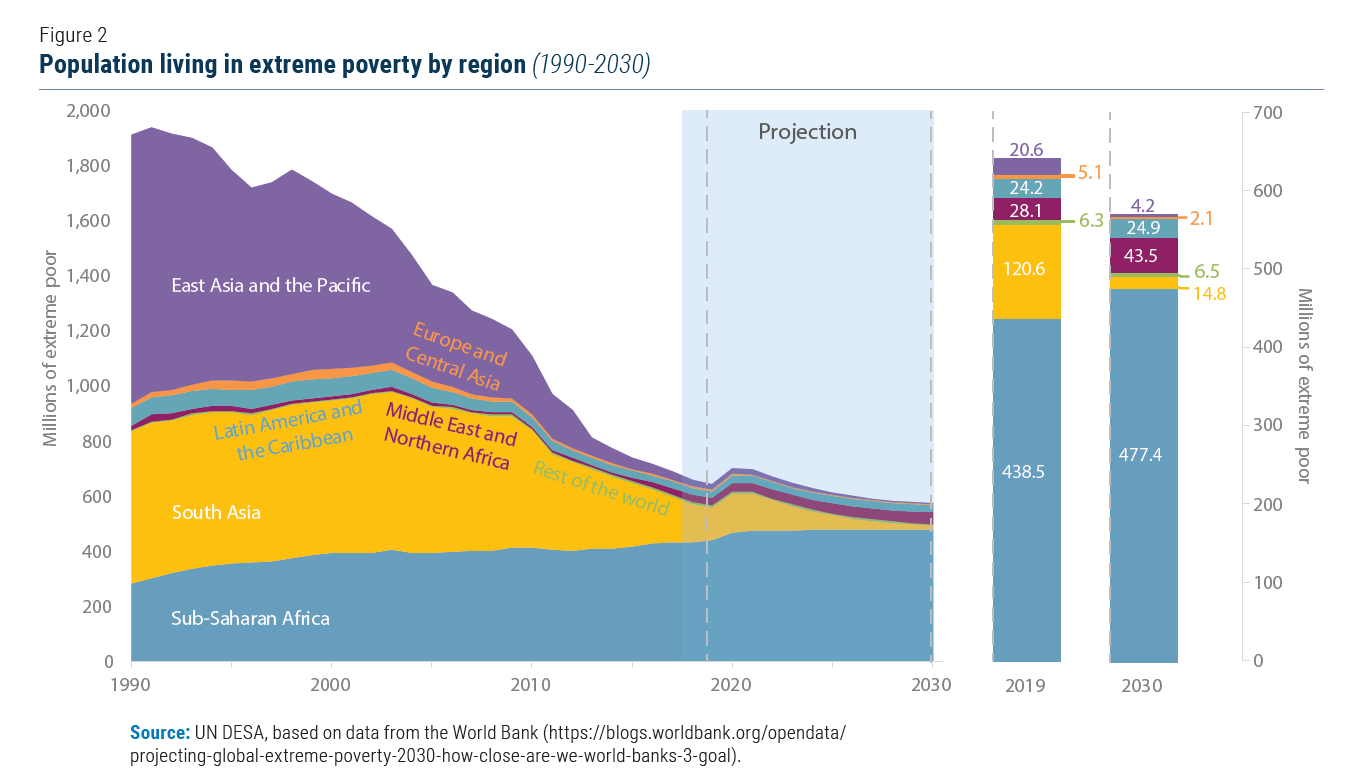

Least developed countries were more severely affected by the pandemic given their less diversified exports and higher dependency on commodities (UN DESA 2021b). LDC exports of goods decreased by 12 per cent in 2020, as mentioned earlier. The value of commercial services in LDCs declined even more sharply, or by 35 per cent in 2020, while in the rest of the world the decline was 20 per cent. The war in Ukraine is now aggravating the situation in many LDCs, as they are generally more vulnerable to external shocks, particularly because some are net importers of food and energy. In these countries, it is expected that the compounding effects of these shocks may have long-lasting negative effects on different dimensions of sustainable development. Within countries, individuals and households are also affected to different degrees. COVID-19 started a vicious cycle whereby disadvantaged groups were not only more exposed to immediate risks from the pandemic, but also less prepared to cope with the financial burdens of the lockdowns (UN DESA 2021c). Poorer countries are still denied equitable access to vaccines and treatments. In addition, the war in Ukraine, in a worst-case scenario, can cause an additional 11 million people to fall into poverty (UNDP 2022). Rising food and energy prices will disproportionately affect the most vulnerable. These essentials make up a larger share of the consumption basket of the poor, so an increase in their prices disproportionately erodes the real income of such households. They may also have less access to financing options to absorb such price increases. Lower-income households also rely more on wages, transfers, and pensions which typically lag behind price inflation. At the same time, high food prices could increase the returns to agriculture, potentially improving the incomes of those working in this sector. Long-term impacts on children are likely to be severe, particularly in developing countries. It is estimated that 147 million children missed more than half of their in-class instruction during the past two years. The share of 10-year-old children in low – and middle-income countries lacking reading proficiency rose from 59 to 63 per cent, with a similar shift also experienced in math proficiency. This effect will linger as this generation of students could lose $17 trillion in lifetime earnings at present value, the equivalent of 14 per cent of today’s gross world product. They are also getting less support as 65 per cent of governments in low – and lower-middle-income countries reduced their education budget. The 2007-2008 food price crisis also showed how spikes in food prices increased malnutrition among the poor, with lasting consequences. Soaring food prices adversely affected child development through poorer nutrition – potentially leading to irreversible loss in cognitive abilities and other lifelong disadvantages – among households that were not able to produce food for home consumption.  Between-country inequality has increased since 2020, and the war in Ukraine could delay progress on SDG 10. Lower-income countries have been more adversely affected by the pandemic causing higher global inequality (Figure 3). Between-country income inequality, which remained relatively steady since 2015, rose sharply due to the pandemic and is expected to remain above pre-pandemic levels well into the second half of this decade. Scenarios in which a decline occurs are predicated on the expectation that developing countries will in general experience faster economic growth than developed countries, as well as the ability of the international community to effectively deal with the aftermath of the current crises and be more prepared to manage future crises. Inequality—already exacerbated by the pandemic—stands to be further worsened by the rising prices. The overall effect of higher prices on inequality is negative. According to UN DESA estimates, about 910 million people live in countries where income inequality could increase by more than 20 per cent due to a COVID-related inflationary shock, with developing countries accounting for 70 per cent of this number. According to a simulation conducted by UN DESA, a 2 per cent average annual increase in income inequality in developing countries from 2022 to 2030 could increase the global poverty headcount by close to 200 million people by 2030 (UN DESA 2021d).

Between-country inequality has increased since 2020, and the war in Ukraine could delay progress on SDG 10. Lower-income countries have been more adversely affected by the pandemic causing higher global inequality (Figure 3). Between-country income inequality, which remained relatively steady since 2015, rose sharply due to the pandemic and is expected to remain above pre-pandemic levels well into the second half of this decade. Scenarios in which a decline occurs are predicated on the expectation that developing countries will in general experience faster economic growth than developed countries, as well as the ability of the international community to effectively deal with the aftermath of the current crises and be more prepared to manage future crises. Inequality—already exacerbated by the pandemic—stands to be further worsened by the rising prices. The overall effect of higher prices on inequality is negative. According to UN DESA estimates, about 910 million people live in countries where income inequality could increase by more than 20 per cent due to a COVID-related inflationary shock, with developing countries accounting for 70 per cent of this number. According to a simulation conducted by UN DESA, a 2 per cent average annual increase in income inequality in developing countries from 2022 to 2030 could increase the global poverty headcount by close to 200 million people by 2030 (UN DESA 2021d).

The need for investments in the SDGs is rising, as the policy space available in developing countries shrinks

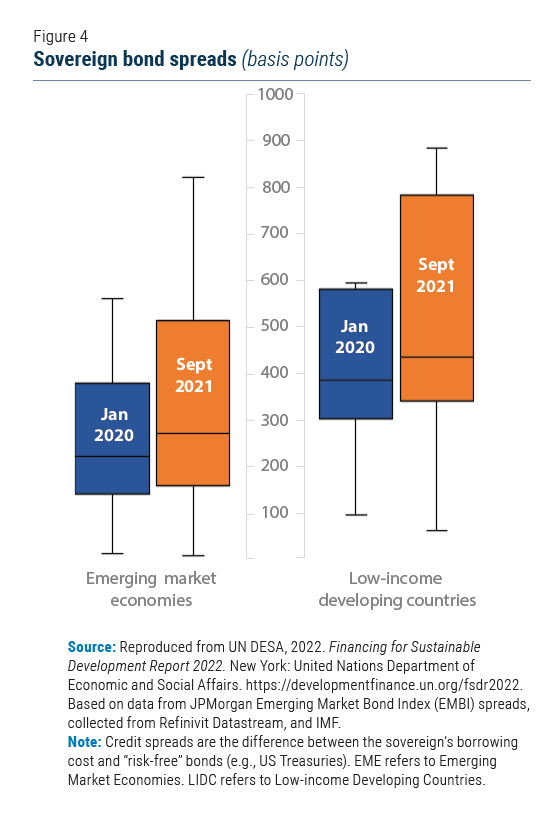

COVID-19 has significantly increased the fiscal costs of achieving many SDGs. Recovering the losses due to the pandemic adds to the investment needs for reaching the SDGs. For example, it is estimated that COVID-19 increased the annual financing gap for achieving SDG 4 in low– and lower-middle-income countries from a baseline of $148 billion by about $30 billion to $45 billion (UNESCO 2020). But investing in remedial and re-enrollment programmes could reduce this additional cost by as much as 75 per cent. The annual spending required to meet the SDGs in five key development areas – education, health, road, electricity, and water and sanitation – could also increase by 21 per cent in select developing countries, compared to the pre-pandemic baseline estimate, up to 2030 (Benedek et al. 2021). The investment required to cope with climate change has similarly increased. It is estimated that capital spending on physical assets for energy and land-use systems in the net-zero transition scenario between 2021 and 2050 would need to amount to about $275 trillion, or $9.5 trillion per year, an annual increase of $3.5 trillion (McKinsey Global Institute 2022). An additional $1 trillion would also need to be reallocated from high-emissions to low-emissions assets in the net-zero scenario. In developing countries, an annual investment of $600 billion would be required by 2030 to limit the rise in global temperatures to 1.65° C, and over $1 trillion to achieve net-zero emissions by 2050 and achieve the 1.50° C pathway by the end of the century. The compounding impact of the recurrent crises has reduced the fiscal space of developing countries. Government revenues in developing countries declined substantially because of the pandemic. In sub-Saharan Africa, total government tax revenue decreased by 15 per cent in 2020 compared to the prior year, a significantly greater decline than during the global financial crisis in 2008-2009 and the Ebola outbreak in 2012. Public debt in developing countries also increased significantly, from 58 to 65 per cent of GDP between 2019 and 2021. Thirty countries in sub-Saharan Africa had a debt-to-GDP ratio exceeding 50 per cent in 2021. The cost of borrowing for emerging market economies and low-income developing economies has also increased substantially compared to pre-pandemic levels and is likely to continue to increase as global interest rates rise (Figure 4).  Shifting fiscal priorities in developed economies also poses a risk to SDG progress and outlook. The war in Ukraine has resulted in rising public expenditures on the military, humanitarian assistance, agricultural commodities and energy supplies in many developed economies. Global military expenditures surpassed $2 trillion in 2021 for the first time and the war in Ukraine has now led to a major reassessment of threat perceptions and military strategies in the advanced economies, particularly in Europe, and expenditures are expected to be significantly higher in 2022. The government of Germany, for example, has decided to raise military spending from 1.3 to 2 per cent of GDP. Increased domestic expenditures in such areas can curtail ODA; this could negatively impact developing countries at a time when their resource mobilization options are limited, and many have already reallocated development cooperation resources from critical SDG sectors, such as infrastructure and education, to address urgent pandemic-related needs (UN DESA 2022c).

Shifting fiscal priorities in developed economies also poses a risk to SDG progress and outlook. The war in Ukraine has resulted in rising public expenditures on the military, humanitarian assistance, agricultural commodities and energy supplies in many developed economies. Global military expenditures surpassed $2 trillion in 2021 for the first time and the war in Ukraine has now led to a major reassessment of threat perceptions and military strategies in the advanced economies, particularly in Europe, and expenditures are expected to be significantly higher in 2022. The government of Germany, for example, has decided to raise military spending from 1.3 to 2 per cent of GDP. Increased domestic expenditures in such areas can curtail ODA; this could negatively impact developing countries at a time when their resource mobilization options are limited, and many have already reallocated development cooperation resources from critical SDG sectors, such as infrastructure and education, to address urgent pandemic-related needs (UN DESA 2022c).

A roadmap to accelerate progress on the SDGs

Recurrent crises lead to cumulative backsliding in SDG progress, compounded by a shrinking capacity to recover, and greater vulnerability to subsequent shocks. Achieving the SDGs in such a context requires focusing on better-designed interventions, proactive efforts to harness new opportunities, and the deliberate development of resilience and the capacity to respond. Global crises pose additional challenges through shocks that are felt worldwide, while potentially limiting the transfers that could be made from developed to developing countries to help mitigate these impacts.

Implement interventions that are more impactful and better targeted

Identify policies with the most impact on the SDGs. Reduced growth due to recurrent crises has directly impacted SDGs and has curtailed the fiscal space available to accelerate SDG progress. In this environment, countries must prioritize those policy interventions with the most impact on SDG achievement given their national context. Policymakers can benefit from the available evidence on the most cost-effective policies for a given sector to decide on how to direct their limited funds. In education, for example, the Teaching and Learning Toolkit gives information on the impact of each intervention option on student progress, as well as the expected cost of each intervention (Pearson 2022). Increase the focus of national and global SDG efforts on those most in need. The uneven progress in many of the SDG indicators means that the bulk of the remaining challenges to eradicating fundamental deprivations is concentrated in some countries and regions. For example, the vast majority of those living under the extreme poverty line will be in sub-Saharan Africa (Figure 2). Since these countries are also those with limited fiscal space and need to devote scarce resources to recover from the recent crises, those efforts to eradicate poverty and accelerate progress in other SDGs must be better targeted to address context-specific challenges and be well supported by the international community. Official development assistance and support for debt relief must be targeted and scaled up, especially for the LDCs. The financing gap of the Access to COVID-19 Tools Accelerator must be closed. While it is crucial to provide support for Ukraine and refugees, resources must not be diverted from developing countries needing both short-term international support for immediate COVID-19 needs and medium– to long-term investments in climate mitigation and adaptation; food security and food systems; social protection; and digital transformation (UN DESA 2022c). International support through public development banks, official debt swaps, rechanneling of unused special drawing rights, and the development of a more comprehensive, long-term solution to address sovereign debt challenges, should also be strengthened.

Harness new opportunities for faster SDG progress

Build on the energy transition momentum. Before the Ukraine war, governments had increased their ambition level for the clean energy transition (SDG 7) (United Nations 2022). Renewable energy solutions and energy efficiency measures together have the potential to achieve 90 per cent of the energy-related carbon reduction needed and 80-90 per cent of global power generation by 2050 (IRENA 2018; UN DESA 2021a). The declining cost of electricity generated from renewables now makes this comparable to that of fossil fuels. Oil demand is projected to peak in the next two to five years due to the rapid development and commercialization of electric vehicles. The spike in oil and gas prices due to the war in Ukraine has strengthened the economic incentives of private and public actors to invest in the adoption of low-carbon energy systems. At the same time, it can also incentivize investments in fossil fuel extraction. Following the war in Ukraine, most major European countries have committed to accelerating the energy transformation, for example, Germany plans to give up coal entirely by 2030, eight years earlier than the previous target. Any temporary measures to deal with fossil fuel shortfalls mustn’t translate into a derailment of the energy transition, or accelerate the depletion of the remaining carbon budget to stay within the 1.5° C aspiration. The digital transformation has the potential to further the achievement of all the SDGs. The spread of digital technologies – accelerated during the pandemic – offers the potential to improve access to and the delivery of services including education, health, finances and public transfers. More broadly, digitalization offers developing countries an opportunity to bypass a traditional structural transformation pathway anchored in the rapid expansion of a highly polluting manufacturing sector to one with a lighter environmental footprint and greater emphasis on growth in services. This is imperative as the global ecological footprint of the current material consumption and production patterns exceeds the Earth’s biophysical capacity by 1.8 times (UN DESA 2020). Social norms are changing, which is furthering the achievement of many SDGs. Young people are particularly at the forefront of a global movement calling for changing lifestyles to combat the impact of climate change and environmental degradation. This has strengthened social awareness and norms aimed at reducing energy use, eating less meat and dairy, cutting consumption, and recycling waste. One-third of the global workforce is also projected to continue to work from home either part-time or permanently post-COVID-19, which would reduce the work-related demand for private and public transport, while business air travel is unlikely to return to the pre-pandemic level. Not every trend has though been positive as was seen by the increase in demand for cars in some countries.

Invest in policy and infrastructure resilience to unexpected events

Recover and expand the national policy space of the most vulnerable countries. Improving governance and public financial management would help countries expand their fiscal space by increasing domestic resource mobilization and lowering borrowing costs. Strengthening institutions and efficacy of public expenditure help investments to deliver value for money and mitigate country investment risks, which would translate into lower borrowing costs. Integrated national financing frameworks (INFF) can help countries align their financing policies and strategies with sustainable development plans and connect holistically to the full range of domestic and international financing sources. Sustain and further strengthen emergency response measures and early warning systems. Analysis of COVID-19 experiences shows that of all the determinants of countries’ performance in dealing with COVID-19, the healthcare system (Goal 3), the social protection system (Goals 1 and 8), and the overall governance system (SDG 16) proved to be particularly important. Many countries – including some of the poorest – also expanded social protection systems. Governments that invest in developing the effective preparedness capacity of these systems are also more likely to enjoy greater public trust, which improves response measures. These efforts should be complemented by more risk-informed development cooperation – both financial and non-financial – that strengthens risk mitigation and resilience-building in developing countries (UN DESA 2022c). Such considerations extend into the multilateral arena, for example through strengthening the global health architecture to better anticipate, prevent and respond to future global health threats. The resilience of multilateral trade should be reexamined in light of the consequences of the crisis-induced disruptions to the global supply chains. On one hand, the easier flows of commodities across the world support resilience when shocks and their effects on supply are localized, as reduced production in part of the global economy can be compensated by supply from elsewhere, provided unimpeded transfers are possible. On the other hand, interdependency and hyper-specialization in global value chains mean that a shock to a central node that produces critical inputs could affect the entire value chain. Similarly, disruptions to part of the global logistic networks can have far-reaching effects. Building resilience into these global interdependencies will require shared incentives to drive the appropriate investments.

Strengthen multilateral cooperation for universal progress and resilience

Official development assistance remains an important component of international financing for development, particularly for the poorer countries. In the least developed countries, for example, ODA accounts for 70 per cent of total external finance. It is important that the fiscal impact of the current crises does not divert attention from the critical role played by ODA in many developing countries and that donors strive to achieve the 0.7 per cent of GNI target. In many developing countries, ODA also plays an important role in leveraging other sources of development financing. There must be a coordinated multilateral response to advance the reform of the international financial system. In addition to increasing development assistance and addressing immediate and long-term debt risks, international cooperation on financial regulation that support financial system stability and alignment of investment with sustainable development is critical. Developing countries should be encouraged to make use of all available policy toolkits, including macroprudential and capital flow management, to address the risk of volatility. Rather than relying on ad hoc responses to shocks, forums for cooperative decision-making on crisis prevention and response should be strengthened before the next crisis hits. The global community should expand the production and equitable access to global public goods, including vaccines. A world where economies and societies are more interconnected also means that shocks are more easily transmitted across borders, and containment is part of a collective response. The Covid-19 pandemic, for example, made it clear that systems of protection need to consider the global context. Global coordination is needed to strengthen research on health threats and treatments, disease surveillance and control, vaccine development and manufacture, outbreak preparedness and information sharing. An immediate need is for current and new vaccines and treatments to quickly be made into global public goods to contain the disease and resume progress towards achieving the SDGs (UN DESA 2021c). In practical terms the global community should continue to strive for all countries to (a) share licenses through the COVID-19 Technology Access Pool; (b) waive intellectual property rights on COVID-19 vaccines through accepted WTO mechanisms, and; (c) expand the vaccine production chain to include developing countries with manufacturing capability.